The 20% tax levy on a Singapore Citizen's portfolio expansion isn't a barrier to entry; it is a sophisticated filter designed to identify investors with the highest conviction in the city's long-term resilience. While many see the current rates of ABSD for second property Singapore as a deterrent, the most discerning capital is already pivoting toward assets that possess the inherent growth potential to absorb these upfront costs. In a market where the Core Central Region continues to lead with a 2.0% growth rate as of mid-2026, the cost of hesitation often outweighs the price of the stamp duty itself.

We understand that the prospect of a 20% or 30% tax liability can feel like an erosion of your initial ROI, especially when coupled with a 45% Loan-to-Value limit for your second mortgage. This guide will empower you to master these fiscal complexities and transform them into a strategic advantage for your 2026 residential investments. We will explore how to identify high-growth assets in District 01 that effectively offset tax friction, provide a clear breakdown of your 2026 liabilities, and outline the financial frameworks necessary to secure a legacy residence in Marina South.

Key Takeaways

- Understand the 2026 tax landscape, including why ABSD for second property Singapore remains at 20% for citizens and 30% for permanent residents to ensure market stability.

- Learn how to calculate your total financial liability by factoring in the revised Buyer’s Stamp Duty (BSD) tiers for luxury assets exceeding the $3 million threshold.

- Discover legitimate pathways for managing tax friction, such as the strategic timing of property disposal to qualify for a full ABSD remission.

- Evaluate why District 01 residences, like the premium 3 and 4-bedroom layouts at One Marina Gardens, offer the capital preservation needed to offset upfront taxes.

- Gain insights into the "Sell One, Buy Two" framework and determine if decoupling remains a viable strategy for your household in the current regulatory environment.

Understanding ABSD for Second Property Purchases in 2026

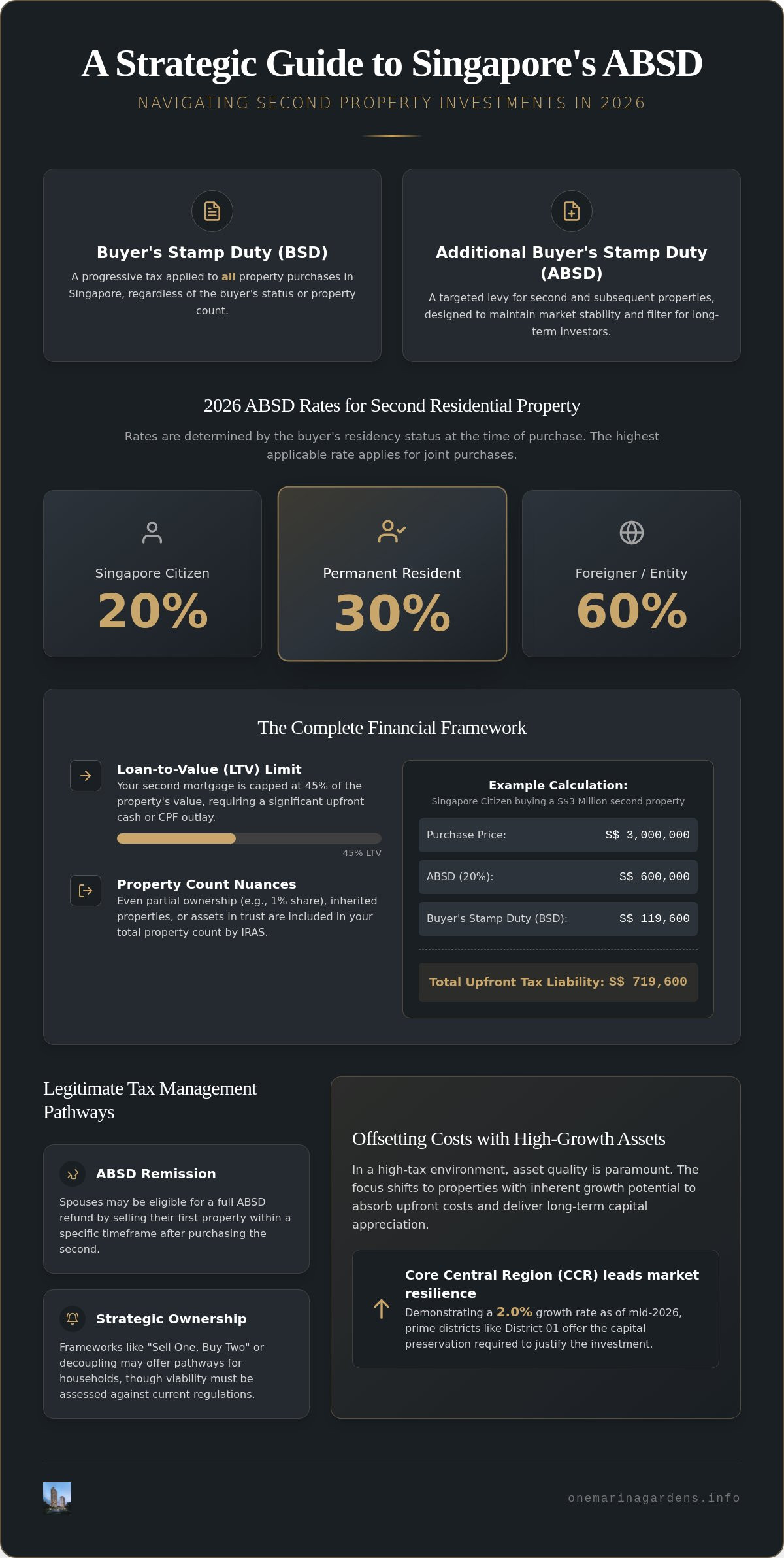

The Singapore residential landscape is defined by its meticulous calibration of stability and growth. Within this framework, the Additional Buyer's Stamp Duty (ABSD) serves as a sophisticated wealth-tiering instrument rather than a mere tax. For those navigating the acquisition of a second home, understanding the nuances of ABSD for second property Singapore is essential for preserving capital and ensuring the longevity of a real estate portfolio. Unlike the standard Stamp Duty frameworks found in other global financial hubs, Singapore’s model is designed to prioritize owner-occupation and curb speculative volatility, ensuring that the market remains resilient even amidst global economic shifts.

While the Buyer’s Stamp Duty (BSD) is a progressive tax applied to all property purchases, the ABSD is a targeted levy that applies based on the buyer's residency status and the number of residential properties they already own. The Inland Revenue Authority of Singapore (IRAS) determines this "count" at the point of the contract date. It's a critical distinction; even a small fractional stake in a prior residential asset can elevate a new purchase into the second-property tax bracket. This mechanism ensures that every acquisition contributes to the broader equilibrium of the city's housing ecosystem.

The Role of ABSD in the 2026 Property Market

In 2026, the government’s commitment to residential stability remains unwavering. The current cooling measures are a response to the sustained demand for premium city living Singapore, where limited supply in prime districts has historically driven rapid price escalation. By maintaining the ABSD for second property Singapore at its current levels, authorities ensure that the market doesn't become overheated by excessive leverage. This creates a more predictable environment for high-net-worth individuals who view Singapore as a safe haven for capital preservation, as it filters out short-term speculators in favor of long-term stakeholders.

Determining Your Property Count

Accurately calculating your property count is the first step in strategic financial planning. IRAS employs a strict approach to ensure the spirit of the cooling measures is upheld. You must consider the following factors when assessing your portfolio:

- Partial Ownership: Owning even a 1% share in a residential property counts as one full property in your tally.

- Inheritance: Inherited properties count toward your total if they are residential in nature, regardless of whether you intended to acquire them.

- Trusts: Properties held in trust for a beneficiary are generally counted toward that beneficiary's property count, impacting their future tax liability.

- Joint Purchases: When parties with different profiles purchase together, the highest applicable ABSD rate is typically levied on the entire purchase value.

This rigorous counting system ensures that the tax remains an effective tool for managing domestic housing demand while allowing the city's most prestigious districts to retain their exclusive allure for serious investors.

ABSD Rates in 2026: Comparing Liability by Buyer Profile

The fiscal landscape of 2026 demands a high degree of precision when expanding a residential portfolio. For Singapore Citizens, the acquisition of a second home triggers a 20% levy, while Singapore Permanent Residents face a 30% charge. This distinction is more than a tax difference; it's a strategic consideration that dictates the entry point for various asset classes. Consulting the latest ABSD rates from official sources is the first step in quantifying the friction involved in ABSD for second property Singapore transactions. These rates reflect a deliberate effort to ensure that those who choose to hold multiple properties are contributing significantly to the nation's long-term urban stability.

For foreign investors, the 60% threshold remains a formidable entry requirement. While this has moderated transaction volume in some sectors, it has simultaneously solidified District 01 as a defensive stronghold for international capital. Only the most exceptional assets are pursued by global investors today, as the high tax barrier necessitates a focus on properties with unparalleled capital preservation qualities. In this environment, the tax isn't just a cost; it's a testament to the exclusivity and enduring value of the Singapore market.

SC vs. PR: The Cost of Portfolio Expansion

The 10% gap between Citizens and Permanent Residents significantly influences the timing of acquisitions. For mixed-status couples, the liability is usually calculated based on the profile with the highest rate, which often necessitates careful legal and financial structuring before committing to a purchase. This tax environment has shifted focus toward assets with high capital appreciation potential, such as an upscale 2 bedroom apartment Singapore, where rental yields and location-driven growth can mitigate the upfront tax burden over a mid-to-long-term horizon. Investors are learning that while the tax is paid once, the benefits of a prime location are harvested for decades.

Entities and Institutional Buyers

Institutional buyers and non-individual entities face an even steeper 65% ABSD rate. This has led professional investors to pivot toward specific asset structures or development-oriented plays that align with the 2026 regulatory environment. The high barrier for entities ensures that housing supply is prioritized for individuals, yet it also creates a unique niche for developers who can deliver high-value residences that justify these institutional costs. Identifying properties that justify these significant upfront costs is the hallmark of a successful 2026 strategy. Discerning investors are increasingly looking toward the curated layouts at One Marina Gardens, where the intrinsic value of a Marina South address provides a robust buffer against tax-driven friction.

Calculating the Strategic Financial Impact on Your Investment

Precision is the hallmark of a successful 2026 portfolio expansion. To accurately assess the viability of an acquisition, you must look beyond the sticker price and model the total capital outlay required at the point of contract. The fundamental formula for your initial tax exposure is the Purchase Price multiplied by the sum of the Buyer’s Stamp Duty (BSD) and the applicable ABSD for second property Singapore. While the Official ABSD rates from IRAS provide the baseline for your calculations, the true strategic impact is found in how these duties interact with your projected capital growth and liquidity reserves.

In the current 2026 fiscal environment, the BSD tiers have been specifically calibrated for high-value assets. For any residential property exceeding the $3 million threshold, the marginal BSD rate is 6%. This means that a premium residence in District 01 doesn't just carry a higher price tag; it carries a higher effective tax rate. When you layer the 20% ABSD for Singapore Citizens or 30% for Permanent Residents on top of these progressive BSD tiers, the total tax friction can exceed 25% of the purchase price. A break-even analysis is therefore essential. If a District 01 asset appreciates at an average of 5% per annum, it will take approximately five years of capital growth to offset the upfront tax duties, making these acquisitions best suited for long-term legacy planning rather than short-term gains.

Many investors focus exclusively on the "tax cost" of buying, yet they often overlook the "opportunity cost" of inaction. In a market where the Core Central Region (CCR) has shown a 2.0% growth rate in a single quarter of 2026, waiting for a policy softening that may not arrive can be more expensive than paying the duty today. A high-growth asset in a prime district often outperforms a lower-taxed suburban property over a ten-year horizon because the superior capital appreciation of the former eventually dwarfs the initial tax savings of the latter.

Total Acquisition Cost Modeling

A comprehensive financial model must account for more than just stamp duties. You should factor in legal fees, which typically range from $3,000 to $5,000 for premium transactions, and mortgage duties if you're securing a second housing loan. These costs, while smaller in scale, impact your immediate liquidity. This upfront friction is exactly why luxury real estate Marina Garden Lane remains a preferred choice for sophisticated capital; the rarity and institutional-grade quality of these assets justify the higher entry costs by offering a more robust defensive play against inflation than mass-market options.

Capital Appreciation vs. Upfront Duty

Historical data from previous cooling cycles demonstrates that District 01 assets possess a unique resilience. Even when cooling measures are introduced, the scarcity of land in Marina South ensures that value remains concentrated. Government expenditure on the Marina South MRT and integrated parklands acts as a fundamental driver for capital gains by permanently elevating the precinct's connectivity and lifestyle appeal. For the strategic investor, the ABSD for second property Singapore is not a sunk cost, it's a premium paid for access to one of the world's most stable and high-performing real estate markets.

Legitimate Pathways for ABSD Management and Remission

Navigating the fiscal friction of property acquisition requires more than just capital; it demands a sophisticated understanding of the regulatory pathways available for tax optimization. While the 20% rate for ABSD for second property Singapore is a standard for citizens, several legitimate mechanisms exist to manage this liability or qualify for a full refund. The most common route is the "Sell One, Buy Two" strategy, which allows married couples to apply for a remission of the ABSD paid on their second property. To qualify, the first residential asset must be sold within six months of the purchase date of the second property, provided it is already completed, or within six months of its TOP date if it is still under construction.

Decoupling remains a viable, albeit more complex, strategy for private property owners in 2026. This involves one spouse transferring their share of a jointly owned property to the other, effectively freeing up one name to purchase a new asset as a "first property" buyer. While this avoids the ABSD for second property Singapore, it's essential to calculate the Buyer’s Stamp Duty and legal fees associated with the share transfer to ensure the net savings justify the move. Trust structures have also gained prominence for legacy planning, though they now require a 65% upfront payment. Remission is only possible if the trust is settled for an identifiable individual beneficiary who does not already own residential property.

Strategic Structuring for Families

Sophisticated investors often preserve their "first property" status by purchasing their initial home under a single name rather than as joint tenants. This foresight allows the other spouse to acquire a future asset, such as an exclusive 4 bedroom premium residence, without triggering the second-property tax bracket. IRAS remains vigilant regarding "nominee" arrangements where a buyer holds a property in name only for another party. These arrangements carry significant legal risks and potential tax evasion penalties; true ownership must always align with the financial reality of the purchase.

FTAs and International Investors

Singapore’s global connectivity extends to its tax treaties. Nationals and Permanent Residents of the United States, Iceland, Liechtenstein, Norway, and Switzerland currently enjoy the same tax treatment as Singapore Citizens due to respective Free Trade Agreements. This allows these specific international investors to bypass the 60% foreigner rate, significantly influencing the Marina South residential development landscape. These buyers typically pay the standard 20% rate for their second property, making District 01 a highly attractive destination for diversified global portfolios.

For those ready to expand their legacy with a high-conviction asset that justifies these strategic maneuvers, we invite you to explore the investment-grade opportunities at One Marina Gardens.

One Marina Gardens: Offsetting ABSD through District 01 Growth

District 01 isn't just a location; it's a financial fortress for discerning capital. While the 20% or 30% ABSD for second property Singapore is often viewed as a hurdle, it's more accurately described as a premium paid for access to the city's most resilient growth corridor. One Marina Gardens stands as the centerpiece of this investment strategy, offering a rare opportunity to acquire institutional-grade assets within the Marina South Master Plan. By leveraging the 99-year leasehold structure, investors can achieve maximum capital efficiency, deploying less initial capital than freehold alternatives while capturing the full appreciation potential of a district undergoing a generational transformation.

The strategic value of an investment in Marina South lies in its ability to outperform the friction of upfront taxes through superior capital preservation. In a market where Core Central Region prices have already shown a 2.0% growth in the first half of 2026, the cost of waiting for a policy shift far exceeds the cost of the stamp duty itself. High-conviction investors recognize that the ABSD for second property Singapore is a one-time entry cost for an asset that will serve as a defensive cornerstone in their portfolio for decades to come.

Investment-Grade Assets in District 01

The proximity to Marina South MRT is a fundamental driver of long-term value, ensuring that residences here remain highly sought after by the city's elite professional class. Within One Marina Gardens, the curated selection of 3-bedroom and 4-bedroom premium residences addresses a significant supply gap in the central region, where large-format luxury units are increasingly rare. These aren't merely apartments; they are supply-constrained assets designed for family legacy and long-term wealth retention. The anticipated completion of One Marina Gardens in 2029 serves as a definitive value catalyst, marking the moment when the precinct's infrastructure and lifestyle amenities reach full maturity and peak desirability.

Securing Your Marina South Legacy

The transition from market research to portfolio acquisition requires a partner who understands the nuances of the 2026 regulatory environment. 2026 represents a critical strategic window for entering the Marina South precinct before the full scale of the Master Plan is realized and entry prices reset to new benchmarks. We invite you to move beyond the complexities of stamp duty calculations and focus on the enduring value of a District 01 address. Your next step toward a sophisticated residential legacy begins with a personalized consultation to align these premium residences with your broader financial objectives.

Securing a Sophisticated Residential Legacy in 2026

Navigating the current fiscal landscape requires a shift in perspective. While the ABSD for second property Singapore remains a primary consideration for portfolio expansion, it's the underlying asset's growth potential that ultimately defines your investment success. By focusing on high-conviction districts like Marina South, you ensure that your capital is positioned to outperform tax-driven friction through superior appreciation and long-term capital preservation. Mastering the nuances of remission pathways and total acquisition modeling is the first step toward a refined investment strategy that prioritizes lasting value over initial costs.

The strategic window to enter the Marina South Master Plan is narrow. Developed by Kingsford Development and offering direct access to the Marina South MRT precinct, the residences at One Marina Gardens represent the pinnacle of District 01 living. These premium 2, 3, and 4-bedroom apartments provide the rare combination of scarcity and strategic advantage required for a modern legacy. We invite you to Explore Strategic Investment Opportunities at One Marina Gardens and align your portfolio with the city's most ambitious urban vision. Your journey toward a resilient and high-status residential future starts with a single, well-considered decision.

Frequently Asked Questions

Can I use CPF to pay for ABSD on my second property?

Yes, you can utilize your CPF Ordinary Account funds to pay for Additional Buyer’s Stamp Duty on a residential purchase. However, the stamp duty must first be paid in cash if the CPF funds aren't disbursed in time, after which you can apply for a reimbursement from your account. It's essential to ensure your CPF balance is sufficient after the mandatory set-aside for your first property’s housing loan remains untouched.

What is the ABSD rate for a Singapore Citizen buying a second property in 2026?

The current rate of ABSD for second property Singapore for Singapore Citizens is 20% of the property's purchase price or market value, whichever is higher. This rate has remained consistent since the April 2023 cooling measures. For a premium residence valued at $3 million, this equates to a $600,000 tax liability, which must be factored into your initial capital outlay alongside the standard progressive Buyer's Stamp Duty tiers.

Is there a refund for ABSD if I sell my first property within 6 months?

Yes, a full refund is available for married couples if at least one spouse is a Singapore Citizen. To qualify, you must sell your first residential property within six months of the purchase date for completed properties or the Temporary Occupation Permit (TOP) date for uncompleted ones. This remission ensures that genuine upgraders aren't unfairly penalized while transitioning between homes in a competitive and highly regulated residential market.

How is ABSD calculated if I buy a property with a mix of SC and Foreigner owners?

When a property is acquired by multiple buyers with different residency profiles, the highest applicable ABSD rate is levied on the entire purchase value. For example, if a Singapore Citizen and a Foreigner purchase an asset together, the 60% foreigner rate applies to the full price. This rule prevents the dilution of cooling measures through mixed-status ownership structures and ensures that all acquisitions contribute to national housing stability.

Does ABSD apply to commercial properties or only residential?

Additional Buyer’s Stamp Duty applies exclusively to residential properties and does not extend to commercial or industrial assets. Commercial properties, such as shophouses, offices, and retail spaces, are exempt from this specific levy regardless of how many residential units you currently own. This distinction makes commercial real estate a strategic alternative for investors looking to diversify their portfolios without incurring the high upfront tax friction associated with the residential sector.

What are the penalties for late payment of ABSD in Singapore?

Late payment of stamp duty attracts significant financial penalties from the Inland Revenue Authority of Singapore. If the payment is delayed by up to three months, a penalty of $10 or an amount equal to the duty payable, whichever is higher, is imposed. For delays exceeding three months, the penalty escalates to four times the original duty. It's vital to settle all liabilities within 14 days of the contract date.

Can I get an ABSD exemption if I buy a property for my child under a trust?

There is no upfront exemption for properties purchased under a trust; you must pay a 65% ABSD rate at the point of acquisition. However, you can apply for a remission if the trust is settled for a specific, identifiable beneficiary who doesn't own any other residential property. This process requires a formal application to IRAS and strict adherence to trust documentation standards to ensure the beneficiary's interests are clearly defined and legally protected.

How does the 2026 ABSD regime impact the rental yield of District 01 condos?

The current tax regime necessitates a focus on net yields rather than gross figures. While the ABSD for second property Singapore increases the total cost of investment, District 01 assets continue to command premium rents that help mitigate this friction. Sophisticated investors prioritize Marina South properties because the high capital growth potential and strong corporate tenant pool in the CBD provide a more robust long-term ROI than lower-taxed suburban options.